Sponsored: Exyn targets safer underground scans

Exyn Technologies Director of Commercial Sales Douglas Minke in conversation with Canadian Mining Journal’s Editor in Chief Dr. Tamer Elbokl during the May 2-5 CIM Connect event in Vancouver. This…

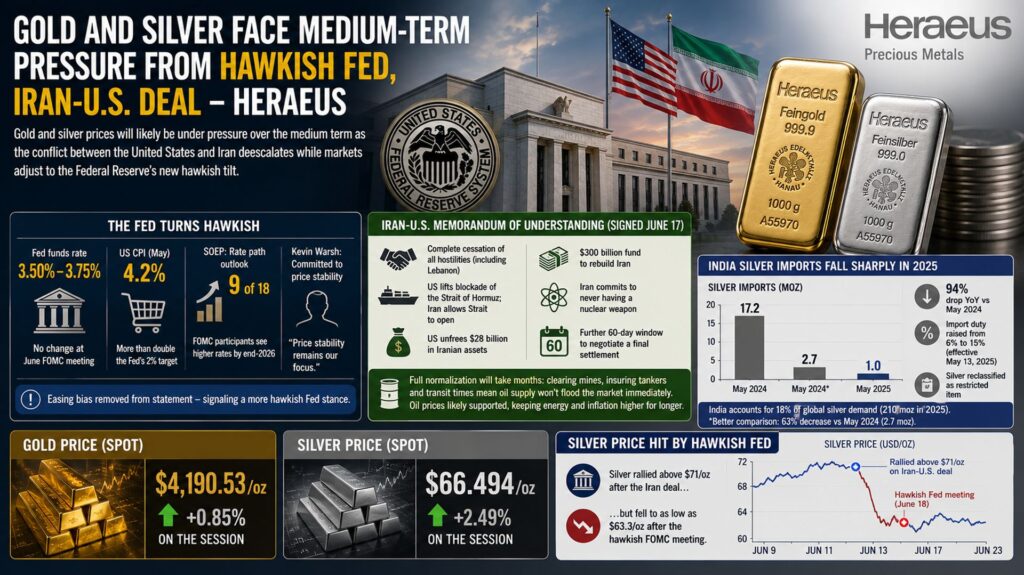

Gold and silver face medium-term pressure from hawkish Fed, Iran-U.S. deal

(Kitco News) – Gold and silver prices will likely be under pressure over the medium term as the conflict between the United States and Iran de-escalates while markets adjust to the Federal Reserve’s new hawkish tilt, according to precious metals analysts at Heraeus.In their latest update, the analysts noted that precious metal prices were shaken up after the Federal Reserve withdrew its easing bias.“Precious metal prices started the week strongly, but although the Fed decided to leave interest rates at 3.5% to 3.75%, the bias to easing was removed from the statement,” they wrote. “This is in line with Kevin Warsh’s ambition to make communication surrounding monetary policy more concise and comes as consumer prices are on the rise, with the US CPI reading 4.2% in May, more than double the Fed’s target of 2%.”“While this should have come as no surprise, there were two other changes from the FOMC meeting that influenced the market’s uncertain reaction,” the analysts said. “Firstly, the Summary of Economic Projections (SoEP) shows half of the FOMC participants believe that the most likely path for near-term interest rates is up, with nine of the 18 participants projecting higher interest rates by the end of 2026 and only one predicting them to be lower.”“Secondly, Kevin Warsh was very keen to stress the Fed remains committed to maintaining price stability,” they wrote. “This part of the dual mandate was spoken about at length, which plays into Warsh’s reputation as a monetary policy hawk. Whether this was just down to the current environment, with elevated energy prices and a change in communication style, or it is a sign of a more hawkish Fed generally is still up for debate.”The analysts also believe the US-Iran conflict is winding down following the signing of the Memorandum of Understanding last week.“The MoU was formally signed on 17 June and contains points surrounding: a complete cessation of all hostilities including in Lebanon, the US lifting the blockade of the Strait of Hormuz, Iran allowing the Strait to open, the US unfreezing $28 billion in Iranian assets, a $300 billion fund to rebuild Iran after the conflict, Iran committing to never have a nuclear weapon, and a further 60-day window to negotiate a final settlement,” they said.But while the conflict may be over, Heraeus expects a full return to normal market functioning will take months.“Although oil through the Strait can theoretically enter the markets now, the practicalities surrounding reopening the Strait might prove significant,” they said. “The clearing of mines and insuring of tankers will take some time and prevent a glut of oil hitting the markets immediately. Then, there is the 4-6 weeks it takes for a tanker to transit through the strait laden with oil and deliver it to its destination. Both of these factors, along with the inevitable rebuilding of stockpiles of oil in the following months, will provide a bid on oil prices that have been heightened since the beginning of the conflict. This, in turn, could keep energy prices higher for longer and influence monetary policy across the globe, with the European and Japanese central banks already having hiked interest rates.”Spot gold has given back some of its earlier gains on Monday morning, last trading at $4,190.53 for a gain of 0.85% on the session.Turning to silver, Heraeus analysts said India’s silver imports have declined dramatically from 2025.“India imported 1.0 moz of silver in May, down from 17.2 moz the year before, making it the lowest of any month since the 0.6 moz imported in February 2023,” they noted. “While the 94% year-on-year drop seems extreme, it is because May 2025 was an outlier with strong investment and industrial demand along with the aftermath of an import duty cut in 2024. A better comparison would be with May 2024 when 2.7 moz of silver was imported. The 63% decrease in imports from May 2024 could be explained by a recent increase in import duty which came into effect on 13 May, raising duties from 6% to 15%. Along with this increase, silver was recategorised as a restricted item, further complicating the import process. India is a significant global silver importer, accounting for 18% of global silver demand which totalled 210 moz in 2025.”And silver prices followed gold lower after Wednesday’s hawkish Fed meeting.“The recent rally in the silver price following the announcement of an agreement between the US and Iran appears to have been stopped in its tracks by a more hawkish Fed committing firmly to maintaining price stability,” the analysts said. “Silver prices rose above $71/oz prior to Kevin Warsh’s first FOMC meeting as chairman, but they have since fallen as low as $63.3/oz. The Fed is likely to remain more hawkish until price indices show clear signs of reducing towards the Fed’s target of 2%. This could continue to subdue the silver price for some time, even as energy prices look set to come down over the coming months following the removal of the blockade of the Strait of Hormuz.”Silver prices are continuing to trade near the top of their daily range on Monday morning.Spot silver last traded at $66.494 per ounce for a gain of 2.49% on the daily chart.

Sponsored: Fortune Bay targets Goldfields PFS milestone

Fortune Bay CEO Dale Verran in conversation with The Northern Miner video host Devan Murugan during The Mining Investment Event of the North in Quebec City. This sponsored video is…

QNI and PSI Announce Engineering Partnership to Support Advanced Nuclear Development

Strengthening nuclear safety, engineering, and regulatory foundations for advanced fuel cycle development at Idaho National Laboratory

IDAHO FALLS, ID, UNITED STATES, June 22, 2026 /EINPresswire.com/ — Quadrant Nuclear Industries Inc. (QNI) and Paschal …

$1.28M in Tokenized Real Estate Sales: Sabai Protocol Tested the Model on the Ukrainian Market

Over the course of 2025, sales of tokenized real estate on Sabai Property passed $1.28M — coming predominantly from the Ukrainian market.

UKRAINE, June 22, 2026 /EINPresswire.com/ — Over the course of 2025, sales of tokenized real estate on Sabai …

Guinea’s president announces ban on raw gold exportsmining.com

“Guinea has the second-largest gold reserves in West Africa,